This article appeared in the Colorado Real Estate Journal's Retail Properties Quarterly on February 17th, 2020 LINK

Retail investor sentiment appears to be slowly improving as recent economic projections indicate a higher probability of a V-shaped recovery commencing in the next few months. The cloud of uncertainty will be hanging around for some brick and mortar retailers longer than others with omni-channel sales. However, some experts are predicting the hardest hit tenants like restaurants and health clubs will come back quickly when occupancy restrictions are fully lifted. Experiential retail is another good example where rapid improvement could result from pent up demand. Most grocery and essential tenants performed well during the pandemic and cap rates on these properties held or declined due to a scarcity of properties on the market combined with lower yields on alternative investments like multi-family and industrial.

Uncertainty with accelerating e-commerce

trends over the past few years reduced lender demand in 2020 and many balance

sheet lenders were over-weighted with retail in their mortgage portfolios well

before the pandemic hit. For example,

CMBS loan pools securitized in 2019 consisted of 40-50% retail. 2021 securitizations are anticipated to have

no more than 20% retail and the collateral will be higher quality with

essential tenants. Lending transaction

activity that did occur consisted of pandemic resistant properties such as QSRs

with a drive-thru, single credit tenants on long-term leases, and grocery and

drug anchored centers with minimal in-line tenant risk. Lending activity in 2021 isn’t anticipated to

increase until pricing discovery occurs combined with demand for higher risk

adjusted returns.

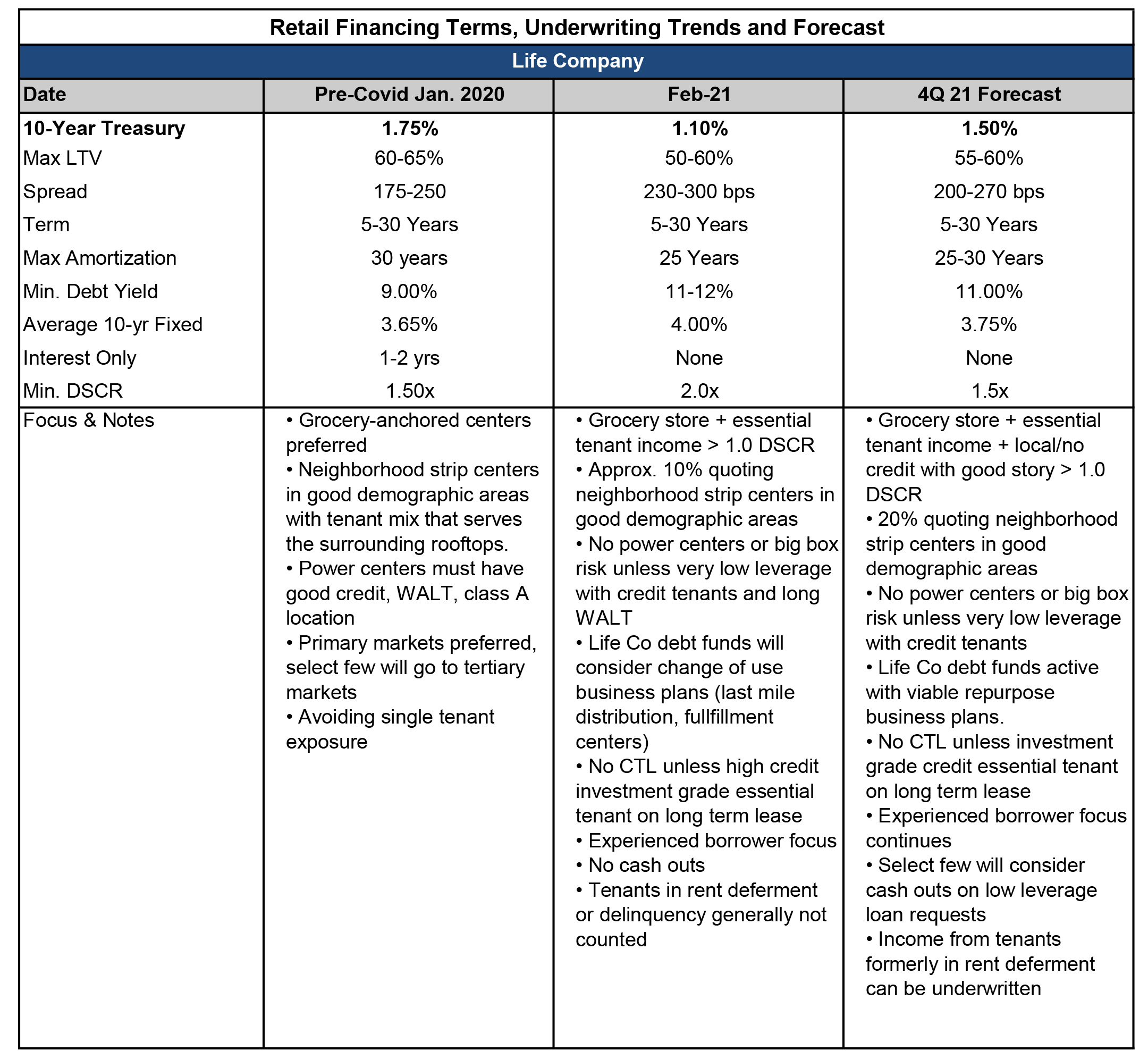

Essex Financial Group has recently surveyed all types of retail

lenders including debt funds, banks, insurance companies, CMBS and private

lenders. Following are some key takeaways:

- A select few insurance companies are currently quoting neighborhood centers with no anchor (non-recourse).

- The majority of all non-recourse lenders are generally avoiding retail without a top tier grocery store anchor included in the collateral.

- All will quote grocery or drug anchored centers with essential tenants. The DSCR typically needs to be 1.0x or higher on combined income.

- Banks require recourse unless very low leverage with essential tenants.

- Several insurance companies anticipate they’ll be back in the market later this year but with more conservative underwriting.

- The herd demand is at an all-time high for industrial and MF. CRE lenders need higher yielding mortgages to increase weighted average portfolio returns.

- Sponsorship experience, financial strength and track record are very important.

- Minimum debt yields are up from 9-10% pre-pandemic to 10-12% (DY = underwritten NOI divided by loan amount) for un-anchored properties.

- Spread premium is 75-100 bps higher on average compared to preferred property types with the exception of grocery and essential tenant anchored centers.

Overall average loan-to-value ratios are down more than 10% compared to YE 2019. However, an improving retail market combined with a fierce competition for preferred alternative property types like industrial are forecast to positively influence retail lending demand through the year. The good news is the doom and gloom at the peak of the pandemic appears to be in the rearview mirror especially in states that have partially lifted indoor dining restrictions. Over the past few months insurance companies have proven to be the best lenders offering non-recourse financing at the highest proceeds and lowest rates. If investors are concerned about interest rates going up in the meantime proceeds are currently available as high as 60-65%.